The Pharmacy Sickness

When Lunds & Byerlys closed all 14 of its pharmacies around the metro area last July, it wasn’t the start of a new trend. It was just the latest fallout from a fundamental change in how the retail pharmacy market functions in the Twin Cities and elsewhere in Minnesota.

Economic forces largely outside the control of pharmacies have replaced supply and demand as the financial lever that decides whether a retail pharmacy stays open or turns off the lights. The potential downside for businesses, employees, health plans, enrollees, and consumers is less choice and higher prices for prescription drugs, not to mention fewer job opportunities for pharmacists, pharmacy technicians, and other people who make their living in the retail pharmacy space.

“It’s a tough marketplace right now,” says Jon Schommer, a professor in the department of pharmaceutical care and health systems in the College of Pharmacy at the University of Minnesota. “Can you survive losing money on every prescription that you dispense? Or do you have another business model that will cover the loss and keep you in business?”

More people, more pharmacies

Schommer has been studying the changes in the retail pharmacy market in Minnesota for more than two decades. In 2018, he and two colleagues quantified those changes in a research article published in the journal Pharmacy.

From 2002 to 2007, the number of retail pharmacies in Minnesota rose 7.4 percent, to 1,070 from 996, and Schommer’s research correlated that increase to population growth—more people, more people with prescriptions, more pharmacies. But population growth didn’t explain what happened during the next two five-year periods.

From 2007 to 2012, the number of pharmacies inched up just 2.2 percent, to 1,094 from 1,070. And from 2012 to 2017, the number of sites actually dropped 2.8 percent, to 1,063 from 1,094. More people, more people with prescriptions, but fewer pharmacies.

“Each successive five-year interval analyzed saw a weakening in the explanatory power of the independent variables of population density and metropolitan designation,” the study said in academic-speak.

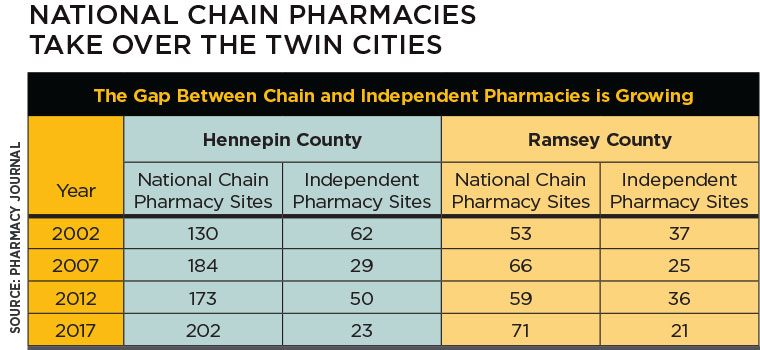

The ratio of chain pharmacies to independent pharmacies also changed over Schommer’s study period.

In 2002, for every national chain pharmacy there was one independent pharmacy, which Schommer defined as a site operated by a single owner or by a small state or regional chain. In 2007 and 2012, that ratio was two to one; by 2017, three to one. Given that the number of pharmacies was relatively flat, independent pharmacies were closing at a dramatic clip.

The ratios were more pronounced in Hennepin and Ramsey counties, at almost nine to one and four to one, respectively (see chart below).

Perverse incentives

The data backed what Schommer, himself a pharmacist, saw happening in the marketplace. In the early 2000s, pharmacies competed for prescription volume and competed on convenience. The more stores they had in convenient locations, the more prescriptions they could fill for customers, and the better their profit and loss statements looked.

“The large corporate chains had a simple business model that said, ‘Hey, let’s just build as many outlets as possible, and let’s put them where the people are,’ ” says Schommer, adding that many independents cashed out and sold their pharmacies to national chains during that period.

Independents rebounded temporarily by competing with the national chains on service and a personal touch. Then, “perverse incentives” entered the ring and knocked out supply and demand and old-school competition cold.

“In what retail markets are you forced to buy something at $6 and then are allowed to only charge $3 for it? There’s only one retail market that does that, and that’s retail pharmacy. It doesn’t make any sense, and it has to change. We’re not asking for the moon.” —Jim Stage, independent pharmacy owner (St. Paul and Hopkins)

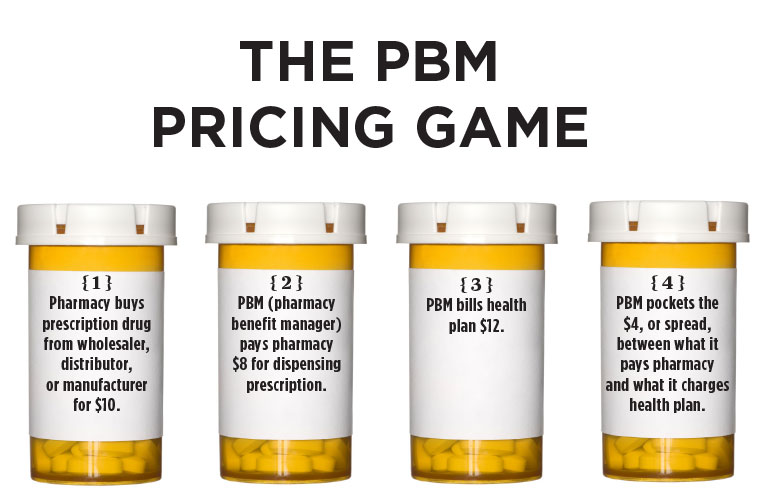

Those perverse incentives (Schommer’s phrase) have all been introduced or at least facilitated by pharmacy benefit managers (PBMs). PBMs are third-party administrators—middlemen—that manage prescription drug benefits for employers or health plans. Through various behind-the-scenes contracting mechanisms with health plans, drug distributors, and drug manufacturers that consumers aren’t even aware of, PBMs can effectively lower prescription drug revenue and raise expenses at retail pharmacies, eating away, if not erasing, profit on their core business of dispensing drugs (see infographic below).

Read more from this issue

A search for independent pharmacies in the city of Minneapolis could identify only two still in business.

More prescriptions, less revenue

Jim Stage is trying to adjust to this new business reality. Stage, a pharmacist, owns three independent pharmacies in the Twin Cities market: Setzer Pharmacy and Lloyd’s Pharmacy in St. Paul, and Hopkins Center Drug in Hopkins. He also owned Schneider Drug in Minneapolis, which he bought in 2015 and sold in 2019. That location is now closed.

“We have more business than we’ve ever had before, but it doesn’t equate to profitability,” Stage explains. “It just equates to more work.”

Setzer, Lloyd’s, and Hopkins collectively fill about 30,000 prescriptions each month, Stage says, and that number has grown steadily over the past five years as other independents close and customers move their prescriptions to Stage’s three stores. But those prescriptions aren’t as valuable as they were five years ago because the payment rate per prescription continues to drop.

Stage laid the blame squarely at the feet of PBMs as his financial torturers.

“In what retail markets are you forced to buy something at $6 and then are allowed to only charge $3 for it? There’s only one retail market that does that, and that’s retail pharmacy,” he says. “It doesn’t make any sense, and it has to change. We’re not asking for the moon.”

High costs, more closings

Stage says he wasn’t surprised when he heard about the Lunds & Byerlys closings or the announcement four months later by HealthPartners that it was closing its 30 retail pharmacies. All HealthPartners sites will shut down by April 1, the Bloomington-based health system said.

“Consumer preferences and pharmacy economics have changed … to favor large-scale organizations able to support extended hours, drive-through pickup, and other conveniences we’re not able to offer,” HealthPartners said in a press release. “Like others preceding us in our market, we’ve made the difficult decision to exit our retail pharmacy operation.”

HealthPartners closures cost 300 positions, including about 100 pharmacists.

Stage says the pharmacy operations at Lunds & Byerlys and at HealthPartners likely had cost structures and low- or no-cost services supported by the prescription drug revenue that they were generating at the time. But once that revenue started to dry up thanks to PBMs, they had to make some difficult decisions.

By creatively contracting with health plans, drug distributors, and drug manufacturers, PBMs can set the prices pharmacies pay for drugs and the prices that pharmacies get paid for drugs, with PBMs taking a cut at each end of every transaction. That difference for retail pharmacies means a small profit at best or, more often than not, a small loss on each prescription filled (see chart).

A study released in January by the Berkeley Research Group, an Emeryville, California-based consulting firm, and sponsored by PhRMA, the trade group representing drug makers, said 54.3 percent of total spending on brand-name drugs in 2018 flowed back to drug companies. The rest went to health plans, PBMs, federal and state governments, employers, drug distributors, providers, pharmacies, and others. The study said nearly half of the increase in spending from 2015 to 2018 flowed to payers, including PBMs.

HealthPartners declined an interview request from Twin Cities Business as did the Minnesota Society of Health-System Pharmacists.

Out from behind the counter

“Price is a problem, but that problem lies outside of the pharmacy,” says Jessica Astrup. Ironically, the answer to the problem also lies outside of the pharmacy or at least away from the pharmacy counter.

Astrup’s grandfather founded Sterling Pharmacy, a regional pharmacy chain, in 1952. Sterling is based in Austin, 100 miles south of the Twin Cities. It operates 17 retail pharmacies along with four pharmacies in long-term care facilities, and one specialty infusion pharmacy for patients receiving intravenous treatments like chemotherapy or immunotherapy. Astrup’s father and uncle, both pharmacists, own the chain now along with her and her siblings. Astrup sits on the board and is part of the management team.

Astrup agrees that PBMs have disrupted the traditional economic forces that drove the retail pharmacy economy in the past. Not only are PBMs pushing down payment rates for prescriptions, she says, they’re stealing prescription business from local community pharmacies by steering customers to national chain pharmacies they are affiliated with, or their own mail-order pharmacies.

“They’re driving out competition and limiting patient choice,” Astrup says.

The National Association of Chain Drug Stores referred questions to the Minnesota Retailers Association, which did not respond to several interview requests.

Pursuing a new business model

Community pharmacies like Sterling can’t compete by being fast, accurate, and cheap. Those are table stakes, Astrup says, and pharmacies have to do more to stay in business today and to be successful in the future.

Specifically, independents in the Twin Cities market need to reinvent their business model by expanding clinical services, better serving employers and personalizing their services to meet the diverse needs of the local population, Astrup explains.

“Pharmacists shouldn’t be spending their time comparing pictures of pills on a screen with actual pills in a bottle,” she says. “Instead they should be spending their time away from the pharmacy counter and in front of patients ensuring that the patient’s health—physically, mentally, emotionally, and spiritually—is being addressed by their health care team.”

Additional services can create new revenue streams for independent pharmacies as health plans may reimburse those as covered medical benefits or employers may pay directly for them as employee benefits.

Sterling is part of the Community Pharmacy Enhanced Services Network, a national network of pharmacies that focuses on direct patient care and advocates for health plan coverage of direct patient care services provided by pharmacies and pharmacists. Sterling also won a grant last October from a program called Flip the Pharmacy that helps pharmacies transition from a prescription-dispensing business model to a patient-care business model by becoming proficient in:

- Leveraging an appointment-based model

- Improving patient follow-up and monitoring

- Establishing working relationships with other care team members (doctors, etc.)

“I believe we are on the cusp of significant innovation in community pharmacy in the Twin Cities,” Astrup says.

Lobbying for market-based reforms

Getting out from behind the pharmacy counter doesn’t just mean seeing patients. It means seeing state legislators, too.

Independent pharmacies working with myriad groups got legislation passed in 2019 that will regulate PBMs in Minnesota.

Gov. Tim Walz signed the bill, known as the Minnesota Pharmacy Benefit Manager Licensure and Regulation Act, which took effect Jan. 1. The law gives the Minnesota Department of Commerce the authority to license PBMs and, starting June 1, to require them to file annual reports detailing their business and contracting practices.

CBD may ease some of the pain

Retail pharmacies in the Twin Cities and throughout Minnesota also are getting a market-based boost from the Minnesota Board of Pharmacy, which helped draft a new state law that legalized CBD products for human consumption if they meet certain quality controls and labeling requirements. Pharmacists can now sell CBD products, opening up a potential new business line and revenue source for retail pharmacies.

Astrup said Sterling already has decided to start selling CBD soon. “Pharmacies have to find ways to sell more stuff, and preferably stuff that isn’t impacted by decreasing margins,” she says. “More importantly, our patients are curious about CBD, and pharmacists have done a lot of research to get educated about it. We have a level of knowledge about CBD that goes far beyond what the guy at the gas station might have.”

Stage says he’s decided not to offer CBD products at his pharmacies in St. Paul and Hopkins.

Easing administrative burdens

More market-based aid from the Minnesota Board of Pharmacy may come in the form of administrative simplification. Last year, the board began a “stem to stern” review of its rules and regulations to identify opportunities to update or eliminate those that no longer serve a useful purpose, according to Cody Wiberg, a pharmacist and executive director of the board. Following the review, the board will run its recommendations past at least two advisory committees for input and then propose its changes through a formal rule-making process.

Wiberg says he hopes some of the less controversial changes will happen this year. But some of the more comprehensive and potentially controversial changes may take another 12 to 18 months. Collectively, all the changes under consideration by the board could mean less time and money spent on paperwork and more opportunities to add new clinical services faster—both of which independent retail pharmacies say are critical to their long-term viability.

The pharmacy market and medication affordability

Drawing a straight line between what’s happening in the retail pharmacy market in the Twin Cities and the affordability of prescription drugs for employers, health plans, and consumers is difficult. But many say it’s there if you look hard enough. One may cause the other; both may be victims of the same economic forces.

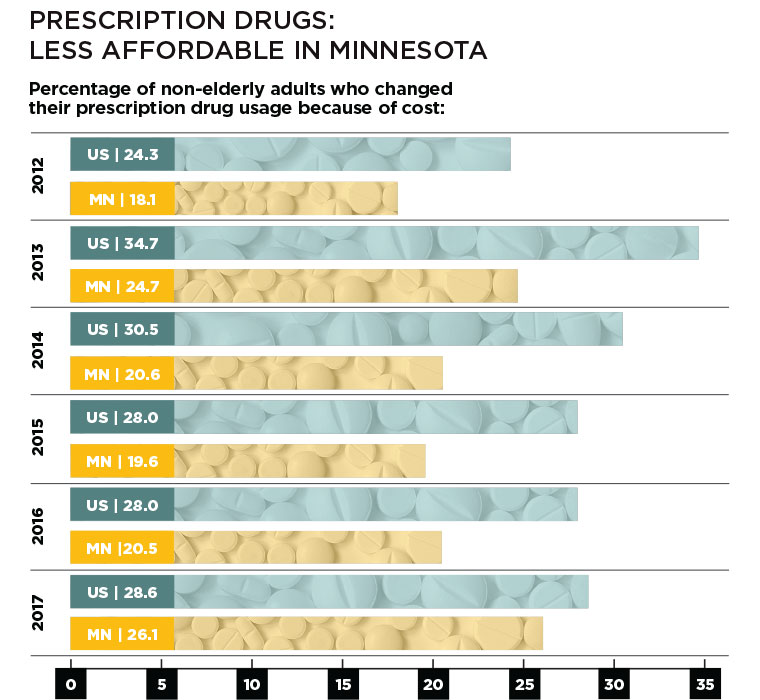

Prescription drugs have become less affordable for Minnesotans over the two most recent five-year periods studied by Schommer and partners, according to data from the State Health Access Data Assistance Center. SHADAC is part of the Health Policy and Management Division of the School of Public Health at the University of Minnesota.

SHADAC tracks drug affordability nationally and by state. It measures drug affordability by the percentage of nonelderly adults who changed their prescription drug-buying habits because of rising out-of-pocket costs for their medications.

Those habits include:

- Asking the doctor for cheaper medications

- Delaying refills

- Taking less medication than prescribed

- Skipping dosages

- Using alternative therapies

- Buying medications out of the country

The percentage of nonelderly state residents who engaged in one or more of those behaviors rose to 26.1 percent in 2017 from 18.1 percent in 2012, narrowing the gap between the state and the nation (see chart).

Health plans shrug

Rising prescription drug costs also are a big concern of the Minnesota Council of Health Plans, which represents commercial health insurers in the state. The council blames rising drug costs on the lack of transparency of drug prices and efficacy, laws that mandate prescription drug benefits and coverage, direct-to-consumer advertising, direct-to-physician marketing, and anticompetitive patent protections.

But so far, changes in the retail pharmacy market haven’t made the council’s hit list.

Who owns a pharmacy—a national chain, a state or regional chain, or an individual owner—can be a sign of how much the owner is willing to spend and how much the owner wants to collect. Is the pharmacy under pressure to meet quarterly earnings expectations? Or just meet next month’s payroll and keep longtime employees on the job?

The answers to those questions translate into access, cost, and safety issues for pharmacy customers.

In January, the New York Times published an expose on medication errors at national chain pharmacies because their corporate owners, according to critics quoted, are pressuring pharmacists to drive prescription revenue. The piece cited anecdotes from pharmacies run by CVS, Walgreens, Publix, and Rite Aid.

In 2017, Minnesota lawmakers thought it necessary to pass a law that bars pharmacists from working more than 12 consecutive hours in a 24-hour period. The rules promulgated by the pharmacy board require pharmacies to give pharmacists a 30-minute uninterrupted break if they work more than six consecutive hours in one day. The rules also require pharmacies to give pharmacists at least one restroom break every four hours.

Right now, the council’s primary concerns about retail pharmacies are whether health plan members have access to pharmacy services and whether pharmacies are coordinating their services with caregivers like hospitals and doctors, according to Julia Dreier, the council’s director of research and health policy. The changes in the retail pharmacy market in the Twin Cities and throughout the state haven’t raised any red flags, she says. “No one is saying they have a concern that their members don’t have access to a pharmacy these days.”

The council is supporting state legislation this year that would increase drug price transparency. Under the legislation, prices for new drugs above a certain level and price increases for existing drugs above a certain level would trigger mandatory reporting and financial justification to the Minnesota Department of Health by the drug manufacturer.

That won’t make much of a difference if independent retail pharmacies are successful in moving away from a prescription drug model to one based on direct patient care, expanded clinical services, and other revenue streams. Five years from now, the data will tell the story of whether it worked.

David Burda is a health care business journalist and former columnist for Twin Cities Business.