Supervalu to Sell 5 Chains in $3.3B Deal, Replace CEO

Eden Prairie-based Supervalu, Inc., said Thursday it has struck a deal to sell five of its largest retail grocery brands to an investor group led by Cerberus Capital Management L.P. in a deal valued at $3.3 billion, and Cerberus also plans to buy up to a 30 percent stake in the rest of the company.

Under the terms of the deal, New York-based private investment firm Cerberus, along with a group of real estate firms, will buy 877 stores under the Albertsons, Acme, Jewel-Osco, Shaw’s, and Star Market banners, as well as the associated Osco and Sav-on in-store pharmacies. The group will buy the chains for $100 million in cash, and the deal also includes $3.2 billion in debt.

Cerberus’ partners in the deal include Kimco Realty Corporation, Klaff Realty LP, Lubert-Adler Partners, and Schottenstein Real Estate Group.

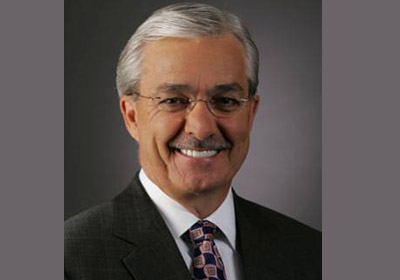

Following the close of the transaction, Sam Duncan will replace Wayne Sales as president and CEO of the much-smaller Supervalu. Duncan, who has more than four decades of retail experience, most recently served as chairman, president, and CEO of Naperville, Illinois-based OfficeMax. Before that, he was president and CEO of ShopKo Stores. Earlier in his career, Duncan held several positions in the grocery industry, including roles at Albertsons; Fred Meyer, a division of Kroger; and Ralph’s Supermarket, a large food retailer in California.

It has not yet been determined whether Sales will remain on Supervalu’s board; if he does not, he will leave the company altogether, according to Supervalu spokesman Mike Siemienas.

When asked how the deal will affect Supervalu’s 125,000 employees, Siemienas said: “The management teams for both organizations will determine staffing needs and roles” for their respective businesses, and “the process could take a couple of months.”

Supervalu will retain its wholesale business; its discount brand Save-A-Lot, which has about 1,300 stores; and its regional grocery brands Farm Fresh, Shoppers, Shop ‘n Save, Hornbacher’s, and Cub Foods, which serves the Twin Cities area. The company doesn’t break out the performance of individual brands in its regulatory filings, with the exception of Save-A-Lot, which saw a 4.1 percent drop in same-store sales during the most recent fiscal quarter.

Following the sale, Supervalu expects to generate about $17 billion in annual revenue. Supervalu is currently Minnesota’s fourth-largest public company based on revenue, which totaled $36.1 billion in its most recently completed fiscal year.

In addition to buying five of Supervalu’s brands, the Cerberus investor group will also buy a stake in what remains of Supervalu. The group will conduct a tender offer for up to 30 percent of Supervalu’s outstanding common stock for $4 per share in cash—which represents a 50 percent premium over its 30-day average closing price as of January 9, the company said.

Shares of the company’s stock were trading up about 13.5 percent Thursday morning at $3.45. Ajay Jain, an analyst at New York-based Cantor Fitzgerald, issued a statement Thursday maintaining his “buy” rating for Supervalu’s stock.

The transactions are subject to closing conditions and also require a fully underwritten refinancing of certain Supervalu debt. (Supervalu said it has negotiated a new $900 million credit facility from Wells Fargo, as well as a separate $1.5 billion loan.) Supervalu expects the deal, which is not subject to shareholder approval because it is a sale of business units rather than the company as a whole, to close during the first quarter of this year.

“The transactions announced today represent the successful culmination of the in-depth strategic review process we commenced this past summer,” Sales said in a statement, adding that the post-sale company will have “three strong, market-leading business units” with more consistent cash flows and improved earnings growth potential.

In addition to replacing Sales—who took the reins last year when Supervalu ousted then-CEO Craig Herkert—Supervalu said it will make other changes to its governance team. Five of its directors will resign, and the new board will consist of five existing Supervalu directors and new directors appointed by the Cerberus investor group, including Albertson’s President and CEO Robert Miller, who will replace Sales as chairman.

Struggling Supervalu—which last year closed stores and cut jobs in a major turnaround effort—began “exploring strategic alternatives,” including a possible sale, in July.

On Thursday, the company reported $7.9 billion in sales for the quarter that ended December 1, down from $8.3 billion during the same period last year. Net earnings totaled $16 million, or 8 cents per share, benefitting from a $26 million after-tax gain related to a cash settlement from credit card companies. In the same period a year ago, the company reported a net loss of $750 million, or $3.54 per share, which included asset-impairment charges of $800 million.

“Key elements of Supervalu’s go-forward business plan include continued focus on right-sizing operations and maximizing efficiencies across the company,” the company said in a statement.

Cerberus, which has more than $20 billion under management, will bring together the Albertsons stores it is purchasing from Supervalu with other Albertsons stores that it acquired in 2006.