Inside the Coffee Shop Business

If you’re under 50, you don’t remember when coffee in America was mostly swill that came from granules spooned into hot water. The term “coffee shop” referenced a daytime diner, a la Seinfeld, where people went for pancakes or a tuna sandwich, whose coffee rarely was something to write home about. But sometime in the 1980s, things started to change. Coffee became an artisanal good, like in Italy or France. Drinking Sanka or Folgers became a sign you were a yokel.

With this evolution came entrepreneurs, notably Starbucks, which picked up on the growing thirst and slaked it, and coffee became a feedback loop that brings us to today, where a small latte sells for $7.40 at a “third-wave” coffee shop.

The coffee cognoscenti describe its evolution in waves. The first was the coffeehouses of the beatniks (1950s-60s); the second was Starbucks and Caribou and the democratization and commercialization of good beans in the ’90s; the third wave was the barista-driven, latte art, specialty coffee era from 2000. Fourth-wave coffee involves a re-democratization of the third wave—coffee shops in the Australian style (friendly and unpretentious all-day cafes with third-wave coffee and a carefully chosen scratch food menu). There’s not much of it in the Twin Cities.

This evolution turned the old coffee shop into an industry category where Americans routinely spend $5-$15 to start their day. The business is full of paradoxes, as packed shops struggle to break even, new entrants emerge quarterly, and consumers decry the spiraling expense but seem powerless to resist it.

Locally Caribou is for sale, Rustica just sold, Dunn Brothers sold recently and wants to quintuple in size, while Starbucks is retrenching. Independents like FRGMT, Spyhouse, Backstory, and Café Ceres are routinely packed, but the latter shut down due to chronic unprofitability. And national drive-thru chains Scooter’s, 7 Brew, and Dutch Bros are eyeing us for expansion.

The business today runs the gamut from tiny one-offs to local chains to large regional and national players. The Twin Cities is not a market the nationals immediately look to, so we tend to see them later in their growth cycle.

The daily ritual

What’s unique about coffee is whereas most of us don’t crave pancakes or tuna salad every day, coffee isn’t optional. “Coffee is emotional,” explains Lee Wallace, owner and CEO of locally based Peace Coffee. “It’s a special daily ritual to people.” As a result, there’s opportunity. “McDonald’s breakfast business was up 20% just on upgrading its coffee,” says Jonathan Maze, editor-in-chief at Restaurant Business, a trade publication. “You can trace that to Starbucks.”

Wallace pinpoints it to about two decades ago, when coffee consumption broadly became “about excellence of coffee and ethical supply chains.”

And then there was the pandemic. “Coffee had a moment during Covid,” explains Erin Newkirk, chief brand and marketing officer for Brooklyn Center-based Caribou Coffee. “It was an essential business. It got you out of the house.” If you hadn’t cared about coffee shops before, now you did.

A good business?

Maze says the pandemic accelerated changes already underway, as second-wave shops spawned variations both downmarket and upmarket. Today the coffee shop business is both mass and small-scale, driven by convenience and an artisan mindset. A few bullet points define common denominators:

- Work from home has remade the industry.

- Workspaces are essential for the one-offs and small chains, as is a welcoming environment that encourages people to bring their work from home to the shop.

- Gen Z customers increasingly want cold drinks and non-coffee products.

- Specialty coffee is the growing segment. Sixty percent of Americans drank specialty coffee last year, says Wallace.

- “All the growth [in coffee] is suburban,” says Maze. “We think of coffee as an urban phenomenon, but now it’s suburban.”

Light roast

Entrepreneurs and investors get into coffee for a variety of reasons, almost always because of their love of the drink, at least initially. But there are business imperatives as well. Daniel Del Prado, who operates some of Minneapolis’ most celebrated restaurants and operated the four-location coffee chain Cafe Ceres, explains, explains:

Coffee has less upfront investment. “You get a lot of tenant improvements [from a landlord]. A restaurant costs a minimum of a million dollars to build out, a basic coffee shop $100,000.” He says percentage of revenue or even free rent is common, making it easier to ride out slow months. “Landlords want [the coffee shop] as an amenity,” he says.

Coffee also promotes loyalty. “It’s a frequency business,” explains Newkirk. “It’s sticky,” adds Wallace. “Once people get into a place, it’s kind of like Cheers—the whole third-place idea.”

And optimally, it’s an appealing place to work. “We have positive, passionate customers, and that really inspires our team,” explains Michael Kollar, a Dunn Brothers franchisee with stores in the west metro.

Dark roast

Despite this, coffee has its downsides.

Del Prado shared some ominous metrics. Wages are up 50% from 2020 in all job categories. Plus, “butter, flour, coffee, milk all has gone up 50% or more in price,” he says. “I can’t charge what I should to make a profit.” He sells a latte for as much as $7.75 but says it should be $11 to generate acceptable margins. Given the absurdity of the situation, he says, “Coffee shops are money pits.”

Read more from this issue

“Coffee shops don’t produce cash flow,” he continues. “Five of them equal one restaurant, and it’s a more difficult worker base,” as he has come to learn.

And the margins are low—“they are low for anything in food,” notes Rustica owner Brent Frederick. “You do it because you love it.”

Rustica’s Lake Street location sits next to a Punch Pizza, which occupies less space but does roughly twice the revenue. “The dirty secret of coffee is it takes an incredible volume to be successful—a line out the door in the morning and busy inside all day,” explains Caribou founder John Puckett, who now is co-owner of Punch. “A store can look busy but not make money. We barely broke even on every college campus.”

Unions have organized various Starbucks around the country, as well as Café Ceres. Puckett theorizes that the intense demands of Starbucks’ volume during Covid uniquely stressed its worker base. But urban coffee shop workers also tend to seek more workplace control. Maze says virtually all unionized non-hotel restaurants are in coffee. But most of the locally based operators TCB talked to said they faced no current issues.

“Labor doesn’t scare us,” says Rustica’s Frederick. “Having a good culture, the right training, scheduling, and benefits helps.”

But the business faces layers of other pressures. Dunn Brothers’ Kollar cites regulatory fees, obligatory retirement plans, and the state’s new paid leave system. Wholesale coffee bean prices have quadrupled in five years due to increased global demand and climate-driven shortages—so retail pricing has risen relentlessly.

Though “we’ve not seen a lot of price sensitivity [among consumers] so far,” notes Peace Coffee’s Wallace, the company chose to get out of the coffee shop business during the pandemic. Wallace says her coffee made at home is roughly 60 cents a cup.

The role of the chew

Most people want food with their morning brew; it’s rare to find a coffee shop without at least a tray of pastries. But most go further, with an array of prepared egg sandwiches and lunchtime fare. For the big boys, it’s all frozen or pre-packaged, but many of the locals cook from scratch. That adds dynamics such as additional training, spoilage, and prep, plus the regulatory burdens that come with fresh food. But woe to the coffee shop that rolls without it.

“Beverages are the profit center,” says Maze. “You sell food to get the beverage sale.” That’s because people don’t want to go to multiple venues, says Caribou’s Newkirk. So “you add food, and you double your sales and add frequency,” says Ben Hertz, co-founder of defunct fourth-wave coffee chain Penny’s. “Come for a meeting, stay to do emails, and at 11:30 you’ll have a salad.”

But where to draw the line? Starbucks has decided its menu is unnecessarily large and is paring back. “The question for us was always how much complexity to add,” Wallace recalls. “Food, cold drinks, alcohol?”

Caribou founder Puckett would draw the line at anything requiring ice: “In my opinion, cold beverages have ruined the coffee business” because they don’t require a skilled barista and are often glorified milkshakes.

The national players

The coffee shop business divides most easily among companies that do business in multiple locations and those based in a single metro area.

Among the big players, smaller-format stores, often without seating but with drive-thru capabilities, are the growth business.

Starbucks is the largest operator of coffee shops in the country, with roughly 17,000 locations. It created the category, by and large, and continues to dominate it. But it is struggling. During the pandemic, with more drive-thrus and better digital capabilities, Starbucks “blew up,” as the kids say—its business exploded, and today it is reaping both the benefits and the drawbacks.

It’s not uncommon to go into a Starbucks and see more than a dozen drink and food items waiting for pickup, or to wait 10-15 minutes for an order in a store with barely any customers. The company also removed seating from stores during the pandemic and didn’t restore all of it. It opened shops designed only for pickup orders. Starbucks admits to hollowing out the hospitality side of the brand and has refocused around restoring that part of its business.

“Customer service data metrics show people don’t like Starbucks, which is driving part of their leadership’s desperation,” Maze explains. “Starbucks has been overwhelmed by mobile.” The company’s new leadership is adapting mobile capacities to control volume while charting a “back to the future” mantra, but “you make money churning customers,” says Maze, who notes that Starbucks hopes for an average of $2 million in revenue per store, which only a handful of the busiest coffee shops in the Twin Cities experience.

Starbucks “can’t turn off the demand that Covid created,” notes Puckett, who says he is watching its evolution closely. Starbucks entered the Twin Cities after Caribou’s 1992 founding—later than it did many metro areas—and we’re one of the few large metro markets the company doesn’t dominate.

The other notable category of national operator is the small-format drive-thru-only business model of 7 Brew, Scooter’s, and Dutch Bros, which are currently the talk of the industry. They are predominantly in suburbs and exurbs. (Scooter’s has a small number of Minnesota locations.)

“The idea of a coffee shop is changing,” says Maze.

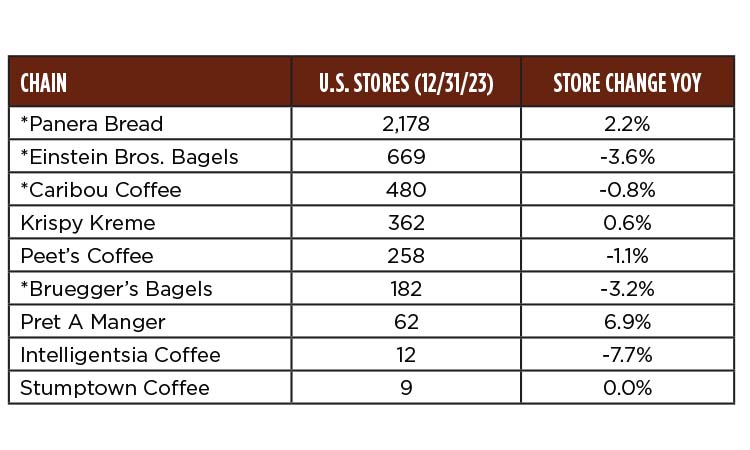

Caribou’s Siblings (JAB Holding Co.)

Source: Technomic Ignite Co.

The locals: Caribou Coffee

Caribou was founded in 1992 by John and Kim Puckett in Minneapolis at 44th and France Avenue South (the location closed in 2023). The Pucketts sold the company in 2000, it went public in 2005, and it was taken private by German food conglomerate JAB in 2012. (Caribou’s history is fascinating but too involved for this feature.) JAB transferred many of Caribou’s stores outside the Upper Midwest to its owned-brand Peet’s Coffee, and Caribou retrenched to the Upper Midwest and a few domestic pockets like Atlanta.

JAB more recently placed Caribou under the umbrella of its St. Louis-based Panera Brands group, along with Einstein Brothers and Bruegger’s Bagels. Last year, Panera announced it was exploring a sale of Caribou and the bagel properties. Caribou’s CEO, John Butcher, announced his departure this March.

Caribou still controls the largest number of coffee shops in the Twin Cities region, but outside observers are uncertain about its trajectory.

“I feel like they’re sort of ignored within JAB,” says Maze. “The parent is very focused on Panera, which is not doing well. I can’t see an obvious strategy to [JAB’s] ownership tenure other than ‘own brands and combine them.’ The Caribous they converted to Peet’s mostly closed.”

Caribou has evolved its strategy over the years. It had long licensed stores in grocery stores, hospitals, and airports, but in 2021 it began franchising stand-alone stores, which is driving current growth back into Michigan and Ohio, plus Florida. Company-owned store growth is in Wisconsin and the Southeast. (Over 40% of Caribou’s stores are franchised in the Arabian Peninsula, North Africa, Turkey, and Bosnia, a legacy of the period before JAB ownership when the company’s largest shareholder was Arcapita, a Bahrain-based investment fund. There are arguably more standalone Caribous in Cairo and Riyadh than Minneapolis.)

Food service advisory firm Technomic Ignite ranks Caribou as the nation’s sixth-largest coffee shop by sales volume. At the end of 2024, it had 487 U.S. locations, 335 of them company-owned. In a franchise disclosure filed for FY23, Caribou said its company-owned full-service coffeehouses with drive-thru (1,500 square feet) averaged $1.08 million in sales, while the drive-thru-only cabin (600 square feet) averaged $806,000, making the economic advantages of the smaller format evident.

“My take is that the biggest factor behind Caribou’s slip in national market share has been the aggressive expansion of its competitors,” says Kevin Schimpf, director of industry research for Technomic Ignite. “Caribou is getting squeezed in both directions by the store growth of bigger players like Starbucks and Dunkin’ as well as the proliferation of smaller upstarts. For context, Starbucks opened over 500 U.S. stores just in the last year.” (Caribou added seven stores in 2024.)

Hertz, the founder of Penny’s, says he perceives Caribou as “gun-shy, risk-averse. They don’t innovate.”

Caribou would, of course, disagree with this characterization. But what’s notable about the company is that as its competitors retrench around coffee basics, Caribou sees itself as more of a coffee-themed hospitality business.

“Caribou is doing what we’ve always done, making people feel like they belong,” says Newkirk. “It doesn’t have to be coffee. Our focus is on where consumers are going.” She describes “meeting guests where they’re at,” with an emphasis on “optionality.”

“There’s the product and there’s the service, the emotional benefit, the gatherings, moments that happen,” Newkirk continues. “We’re there for all of that. … We stay on trend. There’s real lavender on our menu. We’re looking at botanicals, energy drinks that play off the coffee experience.”

Caribou’s founder still sees potential in the company. “I’m sorry to see John [Butcher] go,” says Puckett. “He’d attracted a good team, reinvigorated the culture. Any buyer would want to have him. I think Caribou is still a good business for the right buyer.”

Caribou vs. Starbucks

Caribou: 239 stores (biggest fast-casual chain in the metro area)

Starbucks: 167 data for Twin Cities Metro statistical area

Source: Technomic Ignite Co.

The locals: Dunn Brothers Coffee

Dunn Brothers is a 38-year-old coffee shop business rooted in the Twin Cities. Lacking jazzy branding or an identifiable design signature, Dunn Brothers has always been about the coffee. It roasts its beans in-store, and they are brewed within five days. Its food menu is limited, but the eggs are cracked and the bread sliced right there, compared to the frozen product reheated by the big guys.

Dunn is a franchisor of coffee shops, with only four owned stores. Most stores are in Minnesota, but it also operates in the Dakotas, Wisconsin, Iowa, and Texas. It was sold in 2022 to Gala Capital, a private equity firm based in Orange County, California. Dunn currently franchises 43 stores, down from 54 in 2019. Its 2023 franchise disclosure identified 28 optimized Dunn Bros. with drive-thrus and full menus that averaged $576,000 in revenue, with the best-performing earning just over $1 million.

The company is in the midst of an evolution, says vice president of marketing Alexis Gillette. “Coffee is at our core, but post-Covid we’re rethinking our core. We’re looking at different store formats and footprints, working to grow and create consistency. We’re here to help budding entrepreneurs grow businesses.”

“Quality of coffee is our differentiator,” says west metro franchisee Michael Kollar. “I roast the beans, and our customers give us feedback [on the roast] because they are passionate about coffee.” Kollar’s operation is unorthodox in that he takes less profit and pays staff more because it’s a retirement project for him—but he insists his coffee shops are viable stand-alone businesses: “If my kids wanted to take over my stores,” he says, “they’d live a nice life.”

The locals: The little guys

The Twin Cities is rich in artisanal coffee shops. From Rustica to Spyhouse to Dogwood, they blanket Minneapolis and St. Paul. “The small chains drive the sector forward, like upscale indie restaurants do,” says Maze. “They try new things that filter down. The chains watch them for ideas that work.”

But they may or may not be good businesses.Local restaurant operator Jester Concepts (Parlour, P.S. Steak) recently bought two-unit coffee shop Rustica and announced plans for a third in a defunct Wayzata Wuollet bakery. Jester CEO Brent Frederick says his company, which mostly operates upscale restaurants, got into coffee strategically.

“The bakery drove a lot of it,” and partner Mike DeCamp loves coffee, Frederick says. “On our bakery side, we saw an opportunity for efficiencies and fun integrations with our restaurants.” Jester also found itself overinvested in the inner city after Covid and sees coffee as an antidote. “There’s a path to growth in the suburbs,” says Frederick. “The pandemic exposed us; everything reoriented to the suburbs. Meetings kept happening, but not downtown. We see opportunities in existing coffee shops, such as Wuollet’s awful situation.” (It has been shedding locations due to financial distress.)

It’s worth noting that Rustica once had a million-dollar wholesale bakery business, so at its core, it’s more of a bakery than most coffee shops. Frederick says he hopes to generate at least $1 million in revenue per store.

Del Prado hoped his restaurant chops would deliver a value-add in coffee. When he created Café Ceres, he wanted to grow to 12 units. “It’s an easy business to scale because of low overhead,” he says—assuming you don’t build full-service kitchens (as in the former Penny’s stores he took over). Del Prado and partner Shawn McKenzie lost interest after the shops unionized and the economics of coffee deteriorated.

Though his stores are crowded and lively, he says they don’t break even, whereas his restaurants in the same trade areas do. It’s hard to understand how an operator like Michael Kollar can hit it out of the park in Hopkins and Savage, yet Del Prado can’t in affluent southwest Minneapolis, but that’s the conundrum of coffee.

Percolating…

If you’re wondering where the business is heading, the words one hears most are “automation” and “off-premise.” “Every coffee business is moving toward automation,” says Del Prado. “There are affordable espresso machines today that grind, steam, and do latte art.”

Jonathan Maze adds that “off-premise is the present and future of coffee. The economics of it are compelling.” Chain coffee either wants you to consume in the car or believes you want to.

Both phenomena push the business toward less rent and labor, not to mention mechanized consistency. But the idea of that “third place”—which, in a work-from-home America, so many people seem to crave—seems only a growth engine of Starbucks and the small urban chains.

“It’s funny,” Maze says. “Everyone says they like the idea of that type of coffee shop, it’s just that more and more they are choosing something else.”