The Battle For ShopHQ

Brash billionaire Mark Cuban is a business legend. The owner of the Dallas Mavericks basketball team and a star of TV’s Shark Tank is a hero to many as an independent, self-made man and an outspoken, often irreverent, entrepreneur.

In mid-August, he came to Minnesota to appear on ValueVision’s ShopHQ channel to help nine entrepreneurs whom he’s personally backed sell products on TV. Although the show lasted only two hours, Cuban’s mojo was a shot in the arm for Eden Prairie-based ValueVision Media Inc. The first-ever Mark Cuban’s American Dream drew twice the average viewers for the network, and many of the products sold out quickly.

Could Cuban’s appearance signal a new, higher-profile future for ValueVision?

After a bruising proxy battle led by activist investors, a new CEO took the company’s helm in late June, bolstered by five newcomers to the company’s board of directors. Like a new coach, CEO Mark Bozek—former CEO of HSN Inc., the parent of the Home Shopping Network—is talking a good game about making changes, tuning up the brand and bringing new life to the long-struggling ValueVision.

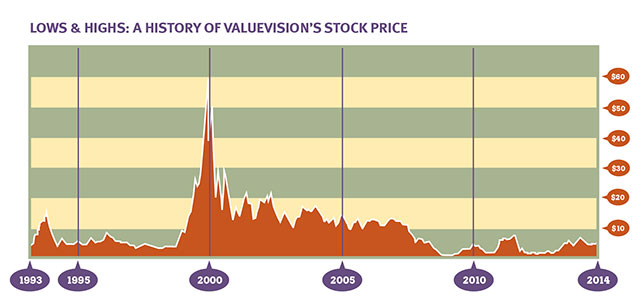

Many local observers and investors have long since written off ValueVision, which is perennially stuck in a distant third place among its television shopping network competitors QVC and HSN. The company has steadily lost millions of dollars for years. Its stock peaked around the turn of the century, reaching $57 a share in late December 1999 before bouncing between $10 and $20 a share for five years, sliding to the bottom at 25 cents a share in January 2009, then rising again but seemingly trapped below $8 a share. This year, it’s bounced between $4.50 and $5 per share since the spring. And the latest plan to reinvigorate ValueVision may sound fairly familiar to those who have watched the company over the last 20 years and seen other touted turnaround plans fizzle.

But there may be more behind the camera than its critics realize. With revenue topping $640 million in 2013, ValueVision is larger than many other, more talked-about Minnesota companies, including Piper Jaffray Cos., Christopher & Banks Corp., Capella Education Co. and Digital River Inc. The company’s programming is being beamed into the cable and satellite systems of 87 million American homes, a platform that would be nearly impossible for a new company to replicate. And it’s growing sales in a very tough environment for retailers everywhere.

When Richfield-based Best Buy Co. announced its second-quarter numbers in August, sales were down 4 percent compared to a year ago. Minneapolis-based Target saw a second-quarter gain of just 1.7 percent. In July the National Retail Federation reported that retail sales grew 2.9 percent during the first half of 2014. Meanwhile, ValueVision posted a healthy gain of 5.4 percent on second-quarter sales. The problem, however, has been making a profit, and that’s where the new leadership team comes in.

Sales for HSN also grew 5.2 percent in the second quarter, while the larger QVC posted a second-quarter increase of 2.7 percent in its sales. But both of those companies are also posting healthy profits.

Mark Argento, senior research analyst with Minneapolis-based Lake Street Capital Markets, likes what he sees so far. He argues that in a challenging retail climate, the third-place status of ShopHQ, known for years under the ShopNBC banner, could have some advantages.

“We think that if they do some of these things right, it could get interesting,” says Argento. “They can experiment. They can try some new things. They can be more nimble. Being No. 3 could be an advantage, especially in a quick-changing market.”

But while the new CEO is talking about the bright, beautiful future, the battle over the future of ValueVision has been long, acrimonious and costly.

ShopHQ: Always in Last Place

ShopHQ has perennially been the third-place player in its industry, trailing the bigger players, QVC Inc. and HSN Inc. Combined, the three companies reported $12.6 billion in sales for 2013. Of that universe, ValueVision accounts for 5 percent.

The West Chester, Pa.-based QVC has more than $8 billion in global sales, with $5.8 billion generated by its U.S. division. The company, which began programming in 1986, reaches 106 million homes in the United States. Combined, QVC channels in Japan, Germany, the U.K. and Italy generated nearly $2.8 billion in sales in 2013.

The St. Petersburg, Fla.-based HSN, parent of the Home Shopping Network, has sales topping $3 billion. HSN traces its programming history to 1981 and reaches 95 million homes. HSN also owns Cornerstone, a collection of lifestyle brands that mails more than 300 catalogues annually and has 11 retail stores. Cornerstone accounted for $1.1 billion in sales last year.

Static from activists

The New York-based Clinton Group might be well known on Wall Street, but the name didn’t mean much in Minnesota until last fall, when the hedge fund targeted ValueVision.

Read more from this issue

The Clinton Group first approached the company in September, but talks soon turned into a brawl that went public Oct. 30, 2013. At that time, the hedge fund issued a letter calling for ValueVision’s then-CEO Keith Stewart, himself a veteran of QVC, to be replaced for leading a company that had underperformed its industry peers. The Clinton Group noted the profits of ValueVision’s rivals, while the Eden Prairie operations generated only red ink. The Clinton Group had amassed a stake of more than 5 percent of ValueVision’s stock. In a letter filed with the U.S. Securities and Exchange Commission, Clinton Group president Greg Taxin did not mince words: “When Keith Stewart, the company’s Chief Executive Officer, joined the company, he declared that he was ‘going to change’ the company’s ‘business model’ and its ‘poor execution.’ Neither has happened. Instead, Mr. Stewart missed nearly every long-term projection and metric he offered during his tenure.”

Stewart took over as ValueVision CEO in January 2009, at what was arguably the low point of the company’s bumpy tenure. The stock was trading for less than $1 per share after a bid to sell the company fell through. In his letter, Taxin was willing to cut Stewart a small break: “The company was in bad shape when Mr. Stewart arrived and he rightly gets credit for keeping ValueVision afloat.”

ValueVision immediately issued its own press release taking issue with the Clinton Group’s claims, and the war of words raged on until the company’s annual meeting June 18 of this year. Shareholders ultimately sided with the activists, and when the dust settled, Stewart was ousted, Bozek was the new CEO and the board had five new members, including Bozek.

“We were contacted originally by a vendor who sells into HSN, QVC and ValueVision,” Taxin says. “He came to us and said having done business with all three of these business over the years, he believed that ValueVision was poorly run.”

Taxin says that he rolled up his sleeves and started looking into the company last summer. As he dug into it, he saw a potentially big upside for ValueVision.

“I think it’s one of the best investment opportunities we’ve seen in a very long time among small capitalization stocks,” he says, noting the breadth of its broadcast platform. “It’s essentially impossible to replicate that distribution. We recognized that there was no reason the company could not exploit that asset.”

But Taxin also saw a business stuck in the past. “I think the business was being run like it was still 1995. We saw it as an undermanaged business that was suffering from a lack of ambition, vision and management prowess.”

Former CEO Stewart and several former board members could not be reached for comment.

Pricey Proxy Fight

The proxy battle was expensive for ValueVision. For its second quarter, ValueVision reported net sales of $156.6 million. But what would have been a small profit of $800,000 for the quarter was instead a loss of $4.3 million due to costs connected to the proxy fight. The company detailed a total of $5.1 million in second-quarter expenses related to the fight: $2.5 million for “activist shareholder response costs” and $2.6 million for “CEO transition costs.”

ValueVision isn’t alone. The muscle of activist investors is stronger these days on Wall Street. High-profile activist investor William Ackman launched a failed proxy battle with Target in 2009, angling to replace CEO Gregg Steinhafel and obtain board seats for himself and others. Ackman ultimately unloaded his Target shares in 2011, and Steinhafel ended up resigning in May following a series of setbacks for the retailer. In a larger national battle, the CEO of the Orlando, Fla.-based Darden Restaurants Inc., parent of the Olive Garden restaurant chain, announced plans to step down earlier this year amid a battle with activist investors.

“I would definitely say there’s an uptick,” says John Potter, a partner in the Minneapolis office of PriceWaterhouseCoopers, on the increase in activist shareholder activity. “We have seen a shift. Shareholder activism is not new. When you take it back over time, you could draw a linkage to the corporate raiders of the ’80s.”

Potter says that in some cases, activist investors can help reinvigorate companies that may have been adrift: “I think there are many good examples where it has created good strategic pivots for companies.”.

Lake Street Capital’s Argento thinks that new CEO Bozek is the right man for the job. “I think he’s an innovator. He clearly was one of the guys that built up HSN to be the company that it is today,” says Argento, noting that Bozek also built up the proprietary brand business for HSN during his tenure: “That’s powerful. Typically the margins are much higher.”

But Argento acknowledges that CEO Stewart helped set the stage for where the company is today: “A lot of the heavy lifting has been done.”

“I think Mark is a fantastic leader and visionary in this industry,” says Taxin. “This company is going to become much more visible in Minneapolis.”

Everything Must Go: A History of Losses

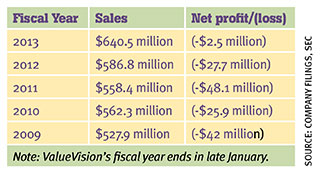

It’s an old joke. A salesman confesses that he loses money on every sale. When his befuddled listener asks how he can possibly make money, the undaunted salesman exclaims: “Volume!” ValueVision has not posted a profitable year in the last five years. The company has posted more than $146 million in combined losses in the same period, while its industry competitors are profitable. But under now-ousted CEO Keith Stewart, the company was cutting its losses and got close to break-even status in 2013. And in a glimmer of hope, the company posted a small profit of $2 million on its 2014 first-quarter sales of $160 million.

Re-Wiring ShopHQ

Mark Bozek believes in the business signals of small details. When he arrived at ValueVision’s headquarters, he discovered a fire extinguisher on the wall directly outside his office. On his second day there, he had it removed. He didn’t like the symbolism.

“It just struck me as being something that was too symbolic of what I didn’t want to be: a fireman putting out fires all over the place. Just metaphorically, it didn’t feel right to me,” he says.

His attention to detail is also apparent in bigger-picture matters: During its second-quarter earnings call in mid-August the company announced it would eliminate its chief operating officer position, tap a search firm to hire a different chief merchandising officer, and open a merchandising and marketing office in New York City.

Bozek has his work cut out for him, and he acknowledges that the company has dropped off the radar of many Twin Cities investors, while falling out of the general public’s awareness as well.

“There’s not a whole lot of people in this town who know who we are, and I aim to change that. I mean, we are a broadcaster in Eden Prairie, Minnesota, in 87 million homes,” says Bozek. “Yet nine out of 10 people that you ask around here have never heard of us.”

Bozek knows the TV shopping business: He was at QVC from 1992 to ’95, and at HSN, where he was CEO, from 1997 to 2003. During his time at HSN, Bozek built numerous proprietary brands into lines generating more than $100 million in annual sales and spearheaded the launch of HSN in Japan, Europe and China.

In a conversation about his vision for the company, Bozek talks about “moving the needle” on the company’s sales, creating a “launching pad” incubator for new personalities and products, and “disruption,” which has become a business cliché.

But Bozek has read the clips. He knows that many long-time observers have heard the same refrain several times before and are likely rolling their eyes and muttering, “Here we go again.” Bozek is squarely focused on a strategy that he says has never been tried: ramping up the volume of proprietary brands on ShopHQ.

“That, to me, has been the missing element for 20 years in this company,” he says. “Our competitors have far more proprietary brands than we do, and that’s the hallmark of what makes these businesses operate. It’s not about the lowest price in town, it’s certainly not about an Amazon play. The real differentiator, the impulse to buy in our world has to come from products you can’t buy anywhere else.”

Bozek sees opportunities for ShopHQ in categories such as home, fitness, cookware, food, vitamins, cleaning, weight loss, beauty and fashion. The company will still sell jewelry and watches, currently its dominant category of merchandise, but he expects that those items will make up a smaller percentage of future sales as new products are rolled out to serve the company’s core demographics, which show that 75 percent of ShopHQ’s customers are women, and about 45 percent of the company’s sales are online.

But Bozek is not looking to run a mini-Home Shopping Network in the southwest suburbs of Minneapolis. “I think following the leaders has been and is still a really bad idea. I was at QVC and I ran HSN. Why would I want to just follow them? I didn’t come here to do that.”

Psst! Wanna Buy a Watch?

No, jewelry isn’t the only thing for sale on shopping television networks. ValueVision Media breaks its sales into four primary categories of goods. As outlined In the company’s second-quarter earnings conference call, sales of fashion items are growing. Sales of home products are also increasing, but sales of consumer electronics are declining.

Looking ahead, CEO Mark Bozek has outlined a plan for a broader mix of goods driven by new proprietary brands that are only available on ValueVision.

April-June, 2014: Sales Mix for ShopHQ

43% Jewelry & Watches

24% Home & Consumer Electronics

18% Fashion & Accessories

15% Beauty, Health & Fitness

Bozek wants to leverage ValueVison’s third-place status by being nimbler than his larger competitors can be, bringing a spirit of experimentation to ShopHQ and making it a televised incubator for products that can’t be found anywhere else.

Mark Cuban is a prime example of the strategy.

Talks for Cuban to appear on ShopHQ were already in the pipeline before Bozek landed at ValueVision. But since the debut of Mark Cuban’s American Dream, Bozek has continued talking to Cuban. A second Cuban show is likely to air on ShopHQ in early October. Notably, Cuban has brought his act to ValueVision, not QVC or HSN.

While looking to raise the profile of ShopHQ, Bozek bristles at the suggestion that he’s looking to put more celebrities on the air. “I’m not a big fan of the term ‘celebrity’—I am much more focused on the notion of personalities,” he says, noting that you don’t have to be famous to have a personality or a great product.

Bozek is also looking to bring back 24-hour live programming to ShopHQ. Currently the network airs 18 hours of live programming and 6 hours of taped programs overnight. Both QVC and HSN are live 24 hours a day. Are there buyers out there in the night?

“You would be surprised at 3 in the morning who is watching TV,” says Bozek.

“Our competitors, obviously, they see it as a reason to stay live. If there wasn’t enough business to be had at 3 o’clock in the morning, they would be on tape as well. … It’s a great opportunity for experimentation.”

But the clock is clearly ticking. Bozek can’t take much credit for the second-quarter results, since he became CEO only a few days before the end of the quarter. The pending third-quarter numbers will be the first results under his management.

“The biggest challenge, I think, always in a public company, is time,” says Bozek.

Waiting for the payoff

In the protracted battle for the future of ValueVision, Cannell Capital LLC of Jackson, Wyo., was another activist investor.

“It’s a work in progress. Change is often good. It’s probably too early to declare it a total victory,” says the firm’s J. Carlo Cannell.

But as he studied the depressed stock price of Value-Vision, Cannell concluded that he saw little downside to the deal and reasoned that making money wouldn’t be any more difficult than “falling off a pancake.”

In his read, Cannell doesn’t think that ValueVision has to grow fantastically to be successful. The key, he says, is to pull profit margins more in line with its larger competitors.

“It really comes down to expanding margins. We think that under the current management and board of directors, ValueVision is going to become increasingly profitable,” says Cannell. “We’re not buying it because we think the revenues are going to double. This is not Twitter. This is a business that has been around for a long time.”

$57per share no more?

Putting Stock in ValueVision?

ValueVision went public in 1991, a year after the company was founded. Over the years, the stock has been on a roller coaster for investors. In December 1999, amid larger market mania, the stock topped $57 per share.

At the other extreme, the stock was trading at less than a $1 per share in late 2008 and early 2009. The stock bottomed out at 25 cents per share. While the company’s shares have rebounded from those depths, the stock has not traded over $10 per share since 2007. It closed at $4.69 at the end of August.

Mark Smith, a senior analyst with Minneapolis-based Feltl and Co., has been following ValueVision since 2011. While he’s encouraged by the new leadership, he says that company watchers will withhold judgment until they see some solid evidence of change.

“Whoever’s running it, you’re going to have to put together a few quarters. … They want to see some results,” Smith says of shareholders. “We like the new CEO, we think Mark can do a good job. It all comes down to execution.”

But Smith says that the time was clearly right for a new direction, underscored by the shareholder vote in June. “There was certainly frustration with management. I think the vote reflected that.”

Argento sees advantages for ValueVision as the industry’s No. 3 player: “They’re the perennial underdog, the perennial No. 3. That’s as much a risk as an opportunity. We’re making a bet here to a degree. I think these guys have one of the most unique platforms available.”

Looking ahead, Bozek sees a lot of “white space” in ShopHQ’s current schedule that can be filled with new ideas, personalities and products. He’s thinking big.

“Minneapolis is perceived as a retail town because of Target and because of Best Buy,” says Bozek. “It’s my hope that it will be perceived as a retail town because of all three of us. Nobody perceives Minneapolis as a retail town that includes us, and I say, ‘Why not?’ ”

Burl Gilyard is senior writer at TCB.