Minnesota Med-Tech 2.0

Minnesota was once the world’s leader in the supercomputer industry with its cluster of company headquarters and hubs including Control Data, Cray Research, Honeywell, IBM and Univac. No longer.

In recent years, some have worried our state’s leadership in medical technology could fade as well.

Behind the scenes, however, captains of this industry have been hard at work adjusting to changing times and reinvigorating this sector of Minnesota’s economy.

World-renowned medical device entrepreneur Manuel (Manny) Villafaña is on the road 60 percent of the time, mostly traveling overseas. “You don’t even want to know how many millions of miles I have with Delta,” he says. “I get on an airplane. They greet me. Everyone knows me because I am traveling so much.”

It isn’t to speak at colleges and universities or symposiums, sharing his knowledge of what it’s like to start up not only one, but three hugely successful med-tech companies. Instead, it’s to hit yet another home run, this time with a company called Kips Bay Medical Inc. At age 74, it’s a hectic lifestyle—perhaps the most hectic he’s seen during a career in the industry that has spanned nearly 50 years. It’s harder than it used to be to grow a med-tech company.

In fact, some argue that the United States—and Minnesota, long considered the mecca for medical device companies—is in danger of losing its status as world leader in this field. Larger industry players are expanding overseas more than they are here; startups face increasingly difficult challenges bringing products to market, hampering their ability to attract investment at home. Foreign investors are increasingly filling that gap and in the process, getting dibs on intellectual property that otherwise would have remained U.S.-owned.

Villafaña agrees there’s reason for concern, but remains steadfast in his belief that Minnesota’s place as the nation’s leader in medical innovation will remain secure for years to come. Sure, times have changed, he says. But launching a new med-tech company has always been challenging.

Industry Titan

Manny Villafaña began his career at Fridley-based Medtronic in 1967, but left to start his own company, Cardiac Pacemakers Inc. (CPI), in St. Paul in 1972. In 1978, Eli Lilly bought CPI, which later became Guidant. Boston Scientific, based in Natick, Mass., purchased Guidant in 2006. Villafaña’s next startup, St. Jude Medical in 1976, is now one of the world’s three largest firms specializing in cardiac pacemakers, along with Medtronic and Boston Scientific. In 1987 he founded ATS Medical Inc., which Medtronic purchased in 2010 for $370 million. In 2007, he started Kips Bay Medical, which he leads today.

“Everyone recognizes how hard it is to start up a medical device company. You have to have a big red ‘S’ underneath your shirt—or blouse if you are a woman—because you have to believe you are Superman,” says Villafaña. “There are so many regulations, so many difficulties raising cash, so much travel. Whatever you do, it has to be done for the worldwide market.”

A survey released in June 2012, conducted by the trade association Minnesota High Tech Association (MHTA) and commissioned by the Medtech Resource Alliance, an Eden Prairie-based group of senior-level executives offering resources to startups, shows that 64 percent of the med-tech CEOs who responded to the survey have an unfavorable impression of their industry, due mostly to concerns about the FDA regulatory approval process.

Does that mean that being an entrepreneur in the med-tech field has lost so much allure that it’s just not much fun anymore?

“Why? Why do you say it’s not fun?” Villafaña asks with a smile full of youthful exuberance. “We are doing a project right now that is potentially bigger than all of the other products I’ve done combined. We are talking about markets that are 10 times bigger than heart valve markets, four times bigger than pacemakers . . . “When a game of golf is more interesting than what I am doing,” says Villafaña, “I’ll take up golf.”

Minnesota still leads

In the 1990s and early 2000s, it was relatively easy for med-tech companies to find investors willing to participate in the three fundamental stages of a company’s development: start-up, follow-on, and merger or initial public offering. Such sources of financing dried up until recently, however (see “Healthy Rebound” sidebar that follows this story), and the industry took a second punch when the FDA toughened regulations on testing and approving new devices, and increased the amount of time needed to earn approval.

Entrepreneurs, investors and industry leaders have since been quoted in local media on how much more difficult it has become to start and grow a med-tech company. What went unnoticed, however, was Minnesota’s situation relative to the rest of the nation: It turned more difficult everywhere, not just here.

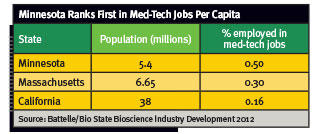

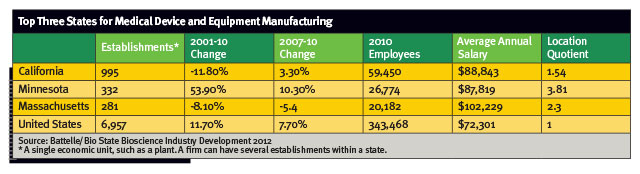

In terms of the number of medical device and equipment manufacturing firms and employees, California ranks No. 1 in the United States. Minnesota ranks No. 2, ahead of Massachusetts, according to a June 2012 Battelle/Bio State Bioscience Industry Development report. And relatively speaking, Minnesota is doing better than other states.

And when it comes to med-tech jobs per capita, Minnesota remains No. 1. Its medical device firms in 2012, the most recent year numbers were available, employed 29,060 people, up 27 percent from 10 years earlier, according to the Minnesota Department of Employment and Economic Development (DEED). These jobs pay an average salary of close to $88,000 a year, according to the Battelle report.

What’s more, Minnesota saw a 54 percent increase in the number of medical device companies within its borders between 2001 and 2010, while California and Massachusetts saw decreases of 12 percent and 8 percent respectively.

That said, a high level of concern remains that Minnesota must do everything possible to retain its title as the nation’s med-tech leader.

“There is no community in the world that has more to lose than we do. If we do not regroup and refocus, we will lose the industry,” says Dale Wahlstrom, president and CEO of LifeScience Alley and its subsidiary, BioBusiness Alliance of Minnesota, nonprofits based in St. Louis Park dedicated to growing and securing Minnesota’s position as a global leader in the life sciences.

Challenge No. 1: Higher hurdles

One reason this industry is so challenged today is because it has already developed its biggest breakthroughs, Villafaña says. That makes coming up with something unique all the more difficult.

“It’s like the old saying: It’s hard to make a brand-new car because cars have been around for a long time. You add innovations to them, obviously, and that’s what we have to do with medical technology. And new innovations are hard to do. Plus, we have a very, very strict regulatory path that we have to go through.”

The changing health care environment, a high turnover rate at the FDA, and the increasing sophistication of medical devices have bogged down the approval process, extending the time to bring a product to market; in turn, these factors increase overall investment needs and lengthen the time that investors must wait to see a return on their investment.

“The regulatory environment over the last decade has certainly been getting more difficult,” says Rich Newitter, analyst with Leerink Swann, a health care investment banking firm in Boston. “A higher level of medical evidence is being requested. The FDA is moving toward requiring more levels of data, more types of studies and more robust levels of clinical evidence.”

The increased stringency, says Newitter, is due, in part, to the shift in the U.S. health care industry, from fee-for-service, in which providers get paid for their volume of work, to a system where payments are linked to evidence-based results.

Novel Class III devices—which support or sustain human life, are of substantial importance in preventing impairment of human health or which present a potential, unreasonable risk of illness or injury—face the longest reviews and clinical trials before being approved for use in the United States. Europe’s review process is much less time-consuming, which is why products are typically approved for use in Europe before use in the United States. China, Singapore and Japan, meanwhile, have set goals to rapidly expand their medical-technology industries using approval processes much faster than in the United States.

In this country, these types of devices require premarket approval (PMA), the most stringent approval process for any medical device. Getting a product through the PMA pathway can take a decade or longer.

Products with a previously approved version, such as a more advanced pacemaker, go through a less stringent approval process called a 510(k) clearance. Yet even the 510(k) regulatory pathway has slowed.

According to Pulse of the Industry Medical Technology Report 2011, a report by EY (formerly Ernst and Young), the average time to clear PMA increased from 15.5 months in 2003-07 to 27.1 months in 2010. As a result, the number of PMAs per year had dropped to only 20 by 2010, compared with nearly twice that many just four years earlier. Meanwhile, the average time for a device to make it through 510(k) clearance increased by about one-third to 4.5 months, while the number of such devices receiving approval each year decreased by about 13 percent to 2,778 in 2010.

And with far more sophisticated devices than those of yesteryear, it takes regulators longer to understand the technology, says Shaye Mandle, executive vice president and COO at LifeScience Alley The more innovative and novel a product is, the longer it will take to get it to market; the more critical a device is to a patient’s health, the more stringent the review. Villafaña has a unique perspective to put all of this into context.

“When I started CPI [Cardiac Pacemakers Inc.], we opened the doors on Feb. 4, 1972. By Nov. 29 of the same year, we already had a human implant of a pacemaker in the United States. There was no FDA formal regulatory approval needed at that time,” he says. “When we did St. Jude, even with FDA approval needed, I opened the doors July 4, 1976, and we did our first U.S. human implant on Oct. 3, 1977. That was with the St. Jude heart valve, a very, very difficult project to do. However, when we did the ATS heart value, it took us, from the time we started the project in 1987 to the time we got approval, 10 years. From the time we did our first human implant overseas to the time we did our first human implant in the United States was five years.”

Today it can take even longer to get a product to market, he says. And that affects the ability to raise capital, as investors have other means of making a return on their funds more quickly.

Challenge No. 2: Additional taxation

Another issue for small medical device firms is the medical device excise tax that went into effect Jan. 1, 2013. Part of the Affordable Care Act, the tax is 2.3 percent of the price of each medical device sold.

“It’s in essence an excise tax, and excise taxes are usually used to kill or reduce things,” as in sin taxes, Wahlstrom says. “If there is to be a tax like this, it should at least be done in a way that is appropriate to a business model. As a sales tax, it is hardest on companies just starting to sell where it may take time to earn a profit.” A tax on earnings would be fairer, he says.

Over the next 10 years, the Congressional Budget Office estimates the medical device tax will bring in $29 billion. Wahlstrom expects Minnesota companies will end up paying between $5 billion and $7.25 billion, or between 20 and 25 percent of the total revenue collected from the tax, and says some companies have decided to bypass the FDA approval process (and tax) altogether by only introducing their products overseas.

“Small companies have to extend credit to their buyers—the hospitals—and they have to pay the tax, so they are out the money they paid in the tax for a period of time,” notes Villafaña.

Companies have had several years to prepare for the tax. “Some restructured in advance to offset the impact of the increase in expenses, while others will bear the burden without cutting costs,” says Newitter. “Some companies will try to pass the cost along to end users. Some have tried to pass the cost off to hospitals, but that is being met with resistance.”

Having the cash on hand to pay the tax and move a product through FDA approval forces most start-up firms to seek additional investors—private, angel, venture and, increasingly, corporate—and to eventually take the firm public or sell it to a larger company. Follow the money

Local investors continued to be interested in companies with new medical technology, though the interest might not be as robust as it once was, according to Dan Carr, CEO of the Collaborative, a member organization that provides growing companies with networking and educational resources primarily centered on raising capital. Within the past year, Carr says, he knows of at least five start-up companies that have raised $10 million to $20 million; he cautions that the drop in capital for startups should be looked at in context—the biggest economic downturn since the 1930s.

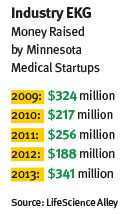

Meanwhile, LifeScience Alley recently conducted a research report that finds investments in Minnesota-based med-tech companies are increasing: $341 million was invested in 92 companies during 2013, an 81 percent increase from the previous year (See “Healthy Rebound”).

According to Wahlstrom, most of this increase is in seed and early-stage financing from a variety of sources, including angel funds that have started up in recent years.

Minnesota’s Angel Tax Credit helped a great deal in this regard, he says. The credit attracts investors by providing incentives to U.S. and foreign investors or investment funds that invest in start-up and emerging technology companies. In 2012, the state gave a total of $11.7 million in angel tax credits to the medical device industry out of a total of $46.15 million, according to DEED.

The challenge now, however, is that as angel investors and funds invest most or all of their capital, they have to wait for a return on their investments. And that requires another level of investment to be made by follow-on investors—typically venture capitalists, private equity funds or larger corporations looking for growth opportunities.

Wahlstrom’s organizations spent much of the last few years encouraging seed-stage investing, but that’s changing. “We’re reducing that activity and are now shifting our emphasis to finding follow-on money.” This includes working with international sources, venture capital firms in Minnesota and elsewhere, and strategic corporate investors.

“The awareness of what’s going on here has spread to elsewhere in the country. They know medical technology is alive and well here.” It has also spread to Asia.

BioBusiness Alliance of Minnesota and LifeScience Alley are pitching opportunities to everyone, from potential investors at firms in Silicon Valley and a French investment company with an office in Georgia to Japanese trade officials and organizations in Singapore that aim to make the country the med-tech gateway to Asia.

“Innovation is catalytic in the sense that it has caught the attention of Singapore, China, Japan and Israel, saying they want to be part of this,” says Wahlstrom. “Money is starting to come in from these countries.”

Foreign investors tend to be willing to wait longer than U.S. investors are for a return on investment, according to Villafaña. “They also tend to acquire rights to the product in return for supplying the capital. It’s a tradeoff: I get capital. You get a license. If I don’t give you a license, I don’t get capital, and therefore everybody loses.” U.S. venture capital firms also have recently opened offices in Minnesota, including Versant Ventures of Menlo Park, Calif. The fund has $1.6 billion in capital under management and has invested more than $40 million in Minnesota early-stage and start-up medical technology companies over the past four years.

Venture capital funds typically invest in high-risk ventures, seeking returns in three to seven years. But given the general slowdown in the regulatory process, the returns on early-stage med-tech firms usually take much longer than in the past and remain riskier than ever. Case in point: Acorn Cardiovascular, a major med-tech start up in Minnesota that was not granted FDA approval and as a result, lost more than $100 million invested in it, primarily by Minnesota investors. That debacle reduced both the ability and appetite of several local investors to invest in additional med-tech plays through 2012.

Meanwhile, funds such as Versant have developed new approaches to successfully investing in med-techs.

One strategy is to purchase early-stage med-tech companies with disruptive technologies (those that could change current medical protocols), help them prove the clinical benefit of the technology, then exit within several years, often before taking the product through the clinical trial stage, says Kirk Nielsen, managing director of Versant’s Minneapolis office and a former Medtronic sales rep.

A recent example: the fund’s 2008 investment in New Hope-based Lutonix, which developed a drug-coated balloon used during angioplasty surgery to treat coronary artery disease. In 2011, Versant Venture exited that investment when New York-based C.R. Bard, a multinational developer, manufacturer and marketer of medical technologies, purchased Lutonix for $225 million.

Another strategy Versant has used investing in medical technology companies is to include a large-cap company with interest in the early-stage technology early in the process by giving the larger firm an option to buy the startup within a reasonable period, often three to five years. Versant Ventures is now discussing possibilities for these types of investments with some of the large medical device firms.

Established, larger med-tech companies “are increasingly looking for added sources of revenue growth while managing every penny. What’s getting cut is research and development, so they’re looking to venture-backed companies to fill their pipeline,” Nielsen says.

After watching the progression of startups in Minnesota for 25 years, Carr figures the state’s med-tech sector will continue to attract investors because of its unique blend of strengths: a base of highly talented engineers and management teams, knowledgeable capital sources and a rich tradition in entrepreneurism and intellectual property formation (which includes a cluster of companies that are innovating and patenting products on a regular basis), as well as lawyers and accountants who specialize in the area, including at the University of Minnesota and Mayo Clinic.

It’s a place, he says, where despite whatever new challenges may come their way, “people will find ways to make things happen.”

Healthy Rebound

Vital signs improve for Minnesota's med-tech industry

By Burl Gilyard

Amid a changing regulatory and health care landscape, industry leaders have complained that raising money for new med-tech companies has become tougher than ever.

“The word ‘brutal’ would be an accurate description,” says Bob Paulson, president and CEO of Maple Grove-based NxThera Inc. “The whole model has fundamentally changed. It’s requiring all of us to rethink how we structure these companies and who you try to partner with right from the beginning.”

Through the 1990s, the Twin Cities was home to more than a dozen brokerage firms that marketed private placement offerings in promising startups and later, taken the best of them public, providing early-stage investors and venture capitalists with, for the most part, a healthy return on their investments. Regulatory changes basically killed this part of the investment banking industry and along with it, Minnesota’s engine for financing startups. And a generation of angel investors—wealthy individuals who are willing to risk a portion of their holdings to back promising concepts—either retired or passed away.

For the first time since then, there appears to be a groundswell of investment support for med-tech and life sciences-related early-stage companies in Minnesota, spanning all kinds of financing for companies innovative enough to find them.

LifeScience Alley, a St. Louis Park-based trade association for medical industry companies, tallied $341 million raised by 92 companies in 2013. That marks a robust 81 percent increase from the $188 million raised in 2012. The LifeScience Alley tally counts venture capital, public offerings, angel and corporate investors. It’s the best showing since the group began tallying local fundraising in 2009.

“Companies are getting a lot more creative. There are more diverse sources of funding,” says Frank Jaskulke, director of membership for LifeScience Alley. “Like water down a river, they’re finding new paths.”

The three most popular sources of financing for Minnesota med-techs today appear to be a new generation of angel investors, large corporations and foreign investors. And the latter source of funding may soon increase further in the area now most needed—follow-on financing.

LifeScience Alley has established relationships with two government-funded agencies in Singapore charged with building a medical technology-driven economy in that country. One is the Agency for Science, Technology and Research, or A*Star, which oversees 14 biomedical sciences, physical sciences and engineering research institutes, and six consortia and centers. The other is SPRING, an agency within the Ministry of Trade and Industry responsible for helping Singapore enterprises grow and for raising awareness of Singapore products and services.

LifeScience Alley also has relationships established with similar organizations in Japan, charged with developing that country’s med-tech industry with the same vigor as was applied to developing its automobile industry and before that, consumer electronics industry.

So who’s recently raised what, and how?

Brooklyn Park-based CVRx Inc. raised $41.7 million in venture capital in 2013 and has attracted a total of $251 million since its inception in 2001. The company’s Barostim Neo is designed to treat hypertension and heart failure, and began selling in Europe in 2012 as a treatment for hypertension. A clinical trial in the United States is also underway.

“The last time we raised money was in July of 2008. . . . It was like day and night, the difference between the two environments,” reflects Nadim Yared, president and CEO of CVRx.

Before the market crashed in fall 2008, Yared says that he routinely got calls from investors who were interested in CVRx. In the latest round, the company strategically pursued investors that are a good fit for the long-term vision of the company.

In a sign of the changing landscape for medical fundraising, investors in the latest CVRx financing round included Spanish venture capital firm Ysios Capital—the company’s first European investor—and Denver-based DaVita HealthCare Partners Inc., a Fortune 500 company.

“Usually when we look for a financing partner, it’s not just about the money. It’s about the skill set that those partners bring to the table,” Yared says.

Jaskulke of LifeScience Alley says that his group is hearing more talk of international investors in Minnesota medical companies, but does not have a way to concretely track those deals: “I know there’s been a number of international investors.”

NxThera, which makes a device that treats enlarged prostate, has fared better than many others in the current climate. The company raised $20.2 million in venture capital in 2013 and had another $3.75 million in commitments in early 2014. Previously, the company announced in October 2011 that it had raised $21.6 million in Series B funding.

“You have to look for nontraditional investors,” Paulson says of the current investment environment. He notes that a private family investment trust took the lead in the latest financing round. He says that he’s also seeing the emergence of “syndicates of investors,” small groups of private investors looking to invest in medical companies.

Paulson knows the business. He was previously the CFO of Endocardial Solutions, which was acquired by St. Jude Medical Inc. for $273 million in 2005. He was then CEO of Restore Medical, which was acquired by Medtronic for $29 million in 2008. He joined NxThera as CEO in January 2009. The company has 29 employees.

Paulson recalls that Restore Medical was one of the last early-stage Minnesota medical companies to go public before the market crash of late 2008.

“The landscape began to change in 2008 and 2009,” Paulson says of the venture capital shift away from med-tech companies. “It just has not come back. . . . It takes longer to get stuff through FDA. It takes more capital.”

Paulson says that the company hopes to be selling its product, Rezum, in the United States by mid- to late 2015: “This [financing] round will take us through FDA clearance.” Eden Prairie-based Sunshine Heart Inc., a publicly traded company, raised $61 million in 2013 through secondary offerings. But the company has taken an unlikely path to both Minnesota and the public markets. The company’s C-Pulse Heart Assist System is an implantable device to treat heart disease.

Sunshine Heart was founded in Australia in 1999 and went public there in 2004. Given the strong med-tech climate in Minnesota, the company opened a local office in 2009 and began migrating its business to Minnesota. Today, the company no longer has any operations in Australia. In February 2012, the company filed to be traded on the NASDAQ stock exchange.

The company raised $21 million in August 2012 through a secondary offering, which was effectively the company’s U.S. IPO. The company raised $15 million in April 2013 and another $46 million in September.

Jeff Mathiesen, CFO of Sunshine Heart, says that the firm’s status as a public company has been an advantage in the current environment.

“We’ve raised over $80 million. We’re looking to have that money get us through our U.S. pivotal trial,” says Mathiesen. “The important thing for us, up until this last raise, [is that] we did not have cash on hand to get us through our pivotal trial.”

Sunshine Heart has about 45 employees. Mathiesen says that the company is looking to start selling its product in Europe in late 2014. It would not be available in the United States until 2017 “at the earliest,” Mathiesen says.

The bottom line? Med-techs need to keep looking beyond traditional avenues to find financing: they’re out there.