Office Vacancies on the Rise

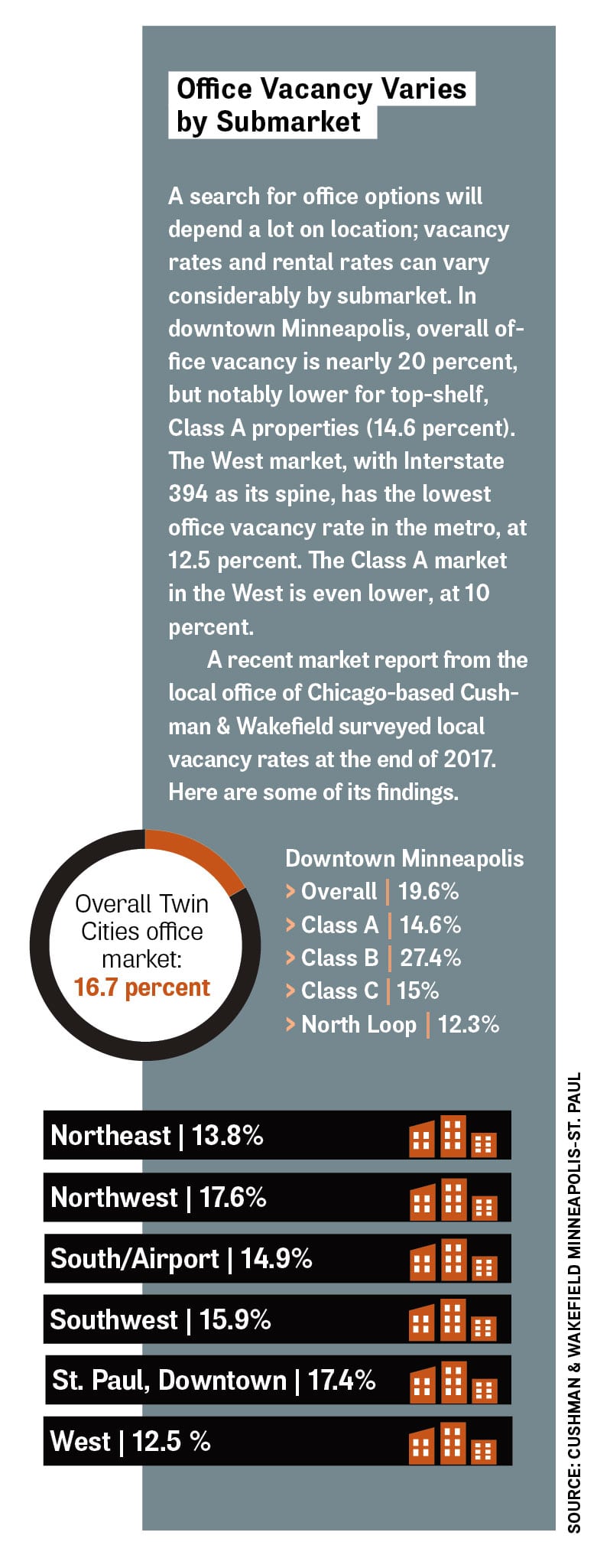

After several years of steady improvement, office vacancy rates are starting to increase again in the Twin Cities. Vacancy rates in downtown Minneapolis are already close to 20 percent and expected to keep climbing. Historically, that’s high. But the post-recession reality is that higher vacancy rates have become the “new normal.”

What does that mean for companies and business owners who are shopping for new space? Do tenants have a chance to cut some sweet deals? Is it worth the hassle and expense of moving to a new building—or is it better to stay put?

“The leverage a tenant has really will vary,” says Jaclyn May, an executive director with the local office of Chicago-based commercial real estate services firm Cushman & Wakefield (C&W). “It’s very much a building-by-building scenario, neighborhood by neighborhood.”

Buildings offering desirable amenities, attributes and locations will often have lower vacancy rates compared to the overall market; those landlords don’t need to offer deals and incentives to draw tenants. The North Loop area of downtown Minneapolis, for example, has been drawing many companies who like the transit connections and energy of the neighborhood, which has a host of new apartment buildings, bars and restaurants.

May also points to the West End area, centered around the intersection of Interstate 394 and Highway 100 in Golden Valley and St. Louis Park, which currently has one of the lowest office vacancy rates in the metro. In the West End, May says, “Tenants don’t have a whole lot of leverage when the vacancy levels are low over there.”

C&W market statistics reported an overall office vacancy rate of 16.7 percent across the Twin Cities at the end of December, but the rate was sharply higher in downtown Minneapolis, at 19.6 percent. C&W’s market research showed 5.3 million square feet of vacant multi-tenant office space in downtown Minneapolis—more room than four IDS Center towers.

The office vacancy rate for Class B properties in downtown Minneapolis was higher still, at 27.4 percent at the end of 2017. It’s a different story in North Loop, where C&W tallied a year-end vacancy rate of 12.3 percent—even lower than the 14.6 percent vacancy rate for Class A properties in downtown Minneapolis.

But market watchers think that office vacancies will climb, particularly in downtown Minneapolis. One reason is several projects in the pipeline, including one by Minneapolis-based United Properties which is developing the Nordic. It will add 200,000 square feet of new office space to the market. That and other projects will add considerable space to the market at a time when tenants’ demand for space does not appear to be picking up.

In the Uptown area of south Minneapolis, the Ackerberg Group, based in Minneapolis, is developing the MoZaic East office building with about 185,000 square feet of office space. The Nordic and MoZaic East are under construction, and space remains available for lease in both. In downtown Minneapolis, the redevelopment team hopes to draw office tenants for 750,000 square feet of space in an overhaul of the former Macy’s store.

Historically, developers waited until office vacancy rates dropped below 10 percent before they considered building new multi-tenant office properties. According to C&W’s statistics, the overall office vacancy rate in the Twin Cities has not been below 15 percent since 2001. Many new buildings have been build-to-suit projects for a single corporate tenant.

The current climate certainly bodes well for tenants, says Mike Salmen, managing principal in the Minneapolis office of Houston-based Transwestern. As tenants weigh staying put versus relocating, Salmen is seeing more companies willing to deal with the disruption in exchange for finding offices with modern amenities, including more open and collaborative space.

“I would say that they’re more inclined to move because they’re looking for a different type of workplace,” Salmen says.

But more empty office space does not necessarily translate into more compelling options for companies.

“Some of the increase in vacancy is space that nobody wants. Some of those out-of-date buildings become less and less desirable,” says Jim Vos, a principal with the Minneapolis office of Cresa, a Washington, D.C.-based tenant representation firm. “The demand for the premier buildings is still pretty good, and the rents are rising.”

Tenancy trends

Two of the dominant themes for tenants today are longer leases and increased construction costs, Vos says.

“The capital requirements to build out new space is forcing everybody to think about a longer lease term. The incentive to spend that money is really to attract talent,” Vos says. “Ten years ago, the cost to build out space was $30 to $40 [per square foot]. Today a lot of people spend $70 [per square foot] without thinking about it.”

Read more from this issue

Longer lease terms can translate into more incentives from building owners. Vos says that in some cases he has seen landlords offering a year of free rent on a 10-year lease. Vos notes that the trend for companies to use space more efficiently and reduce overall square footage per employee continues. He is working with a client looking to trim its footprint by about 20 percent, without cutting staff.

National research shows the metro roughly in the middle of the pack for office vacancy compared to other cities. New York-based REIS Inc., a commercial real estate data and research firm, tallied the national office vacancy rate at 16.3 percent for the fourth quarter of 2017. REIS found Minneapolis with a higher vacancy rate of 17 percent, which ranked 37th out of 79 surveyed metro areas. (Market research studies reflect the same broad trends, but will often have slightly different statistics due to varying methodologies.)

Only three markets are below a 10 percent vacancy rate: New York (8.7 percent), San Francisco (9.8 percent) and Washington, D.C. (9.9 percent). At the other end of the spectrum, many large metros have vacancy rates topping 20 percent: Dallas (21.3 percent), Phoenix (22.4 percent), Detroit (23.2 percent), Las Vegas (23.6 percent) and Memphis (24.3 percent).

REIS found that office vacancy rates increased in 33 of the 79 metro areas that it tracks, noting: “The office market has maintained a sluggish pace of growth throughout this expansion and 2017 was no exception.”

A tenant’s market

“It’s still a tenant’s market,” says Barbara Byrne Denham, a senior economist with REIS.

“The office market in this expansion hasn’t been that robust. Employers are just more conservative with how much space they lease.”

Denham notes that REIS reported the office vacancy rate for Minneapolis at 16.1 percent for the fourth quarter of 2016, but the rate climbed to 17 percent during 2017.

“It is more so a tenant’s market in Minneapolis than it is elsewhere,” Denham says.

But tenants may have to sign longer-term leases to get some extras. Brokers say that landlords are offering richer tenant improvement allowances, which can help offset the costs of renovating and upgrading the interior space.

Construction costs are rising, “so for a tenant to get a decent tenant improvement allowance from the landlord, they need to sign a longer-term lease,” says Mike Brehm, a vice president with the local office of Toronto-based Colliers International.

But not everyone wants an open office. Brehm notes that he has started to see some resistance to the recent trend of open office design. One common complaint is that open office designs can make it harder for employees to concentrate because they are closer together and have less space of their own.

“There has been a little backlash,” Brehm says. “It’s definitely a science on how much open, collaborative space you want.”

Burl Gilyard is TCB’s senior writer.

5 Office Space Trends for 2018 Tenants

-

Construction costs have increased steeply

A big consideration for companies weighing a potential move is that the costs of building out new offices have increased sharply in recent years. But many companies are willing to foot the bill for fresh, modern, appealing work environments.

-

It’s tough to find deals in the best buildings

Yes, office vacancy rates are historically high. In theory, that’s good news for tenants shopping for competitive proposals for potential office space. But the lowest rental rates will likely be found in aging buildings where the landlord has not invested in upgrades and improvements. Is cheaper rent worth the tradeoff for less inviting offices?

-

Longer lease terms are becoming more common

Whereas three- to five-year lease terms used to be commonplace, brokers say that it’s now routine for companies to sign seven- to 10-year deals. One factor: If companies are paying more on the front end to build out the space they want, it makes sense to settle in for a longer stay. Landlords are also more inclined to offer some incentives for tenants making a long-term commitment.

-

Landlords are offering more generous tenant improvement packages

Landlords have been increasing tenant improvement allowances in recent years, which can help offset the higher cost of construction for tenants. A tenant improvement allowance essentially reimburses a tenant for some of the project costs. But companies may need to sign longer-term leases to get larger allowances. Jargon alert: Commercial real estate professionals often refer to tenant improvements as “TIs.”

-

Companies now see office space as a key component for attracting and retaining employees

Real estate used to be seen as a line item on the budget: The company needs to spend X dollars to rent its office space. Today, businesses are looking for inviting venues and amenities that can reflect the company’s culture and help attract and retain employees.

How Much Is This Going to Cost?

The cost of renting an office starts with the net rental rate. The net rental rate is what you pay per square foot leased per year. For example, a net rental rate of $15 per square foot for 5,000 square feet of office space translates to $75,000 in annual rent, or $6,250 per month.

There may be some room to negotiate the quoted net rental rate.

“There’s always a little bit of flexibility,” says Mike Brehm, a vice president with the local office of Toronto-based Colliers International. But he notes that while owners of older buildings without recent improvements might be more inclined to haggle, landlords of newer properties are less likely to budge on quoted rates.

But the net rental rate doesn’t include everything. Tenants also pay costs for operating expenses and taxes, which are essentially passed along from the landlord to tenants. If operating expenses and taxes are $11 per square foot, that adds another $55,000 a year for 5,000 square feet of space. The gross rent would then be $26 per square foot, or $130,000 a year, which does not include any tenant improvements to the space.

There can be big variations between rates depending on location. The average net rental rate in downtown Minneapolis, for example, is almost 50 percent higher than it is in downtown St. Paul.